- The psychology of money starts long before adulthood

- Why smart people still make bad money decisions

- Emotion is often the hidden budget line

- Identity shapes what feels financially possible

- The psychology of money rewards systems, not willpower

- Shame keeps people financially stuck

- How to work with your mind instead of against it

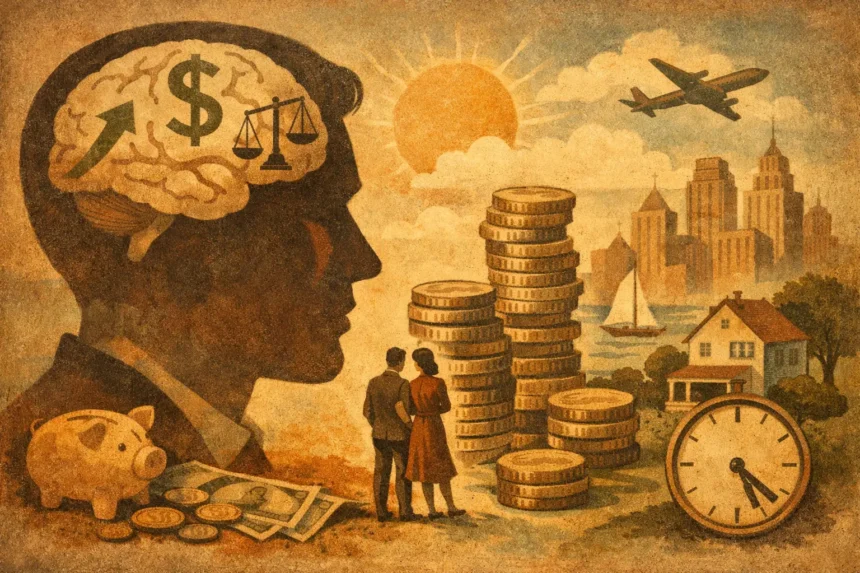

You can know how compound interest works, understand your budget, and still make financial decisions that look irrational from the outside. That is the core insight behind the psychology of money: how your mind controls your financial life. Money decisions are rarely just math. They are also emotion, memory, status, fear, family history, and the stories you tell yourself about what kind of person you are.

That helps explain why two people with the same income can live in completely different financial realities. One saves automatically and sleeps well. The other earns more, spends more, and feels permanently behind. The difference is not always knowledge. Often, it is psychology.

The psychology of money starts long before adulthood

Most people like to imagine they are objective with money. Behavioral science says otherwise. By the time you start earning, your brain has already built a rough money script from childhood.

If money were a source of stress at home, you may associate it with danger, conflict, or scarcity. If it was used to signal success, you may link spending with worth. If your family avoided talking about money altogether, you may have learned that finances are mysterious, shameful, or something to deal with later.

Psychologists sometimes refer to these patterns as money scripts – deeply held beliefs about money that operate in the background. They are not always conscious, and that is what makes them powerful. A person can genuinely want financial stability while repeatedly acting in ways that undermine it because an older emotional script is running the show.

This is one reason financial advice often fails. Telling someone to “just spend less” misses the fact that spending may be doing a psychological job. It may regulate anxiety, create identity, soften loneliness, or produce a quick sense of control.

Why smart people still make bad money decisions

Financial mistakes are not usually a sign of low intelligence. They are often a sign that human cognition has limits.

We discount the future. That is called present bias. A dinner out tonight feels real. Retirement in 30 years does not. Your brain is wired to care more about immediate rewards than distant benefits, which makes saving feel like loss and spending feel like relief.

We also hate losses more than we enjoy equivalent gains. This is loss aversion, one of the most reliable findings in behavioral economics. It helps explain why people hold bad investments too long, panic during downturns, or avoid checking their bank account when things feel shaky. Sometimes not looking feels safer than confronting reality.

Then there is lifestyle adaptation. What once felt luxurious quickly becomes normal. The raise that was supposed to create breathing room gets absorbed into a more expensive baseline. You are not necessarily greedy. Your brain is simply very good at adjusting expectations upward.

None of this means people are doomed to fail. It means better money habits require more than information. They require designing around predictable mental weak spots.

Emotion is often the hidden budget line

One of the biggest myths in personal finance is that emotion is the problem and logic is the solution. In reality, emotion is always involved. The real question is whether you understand what it is doing.

Some people spend when stressed because buying creates a brief hit of reward and agency. Others save obsessively because having money untouched feels like safety. Neither pattern is fully rational nor irrational. It depends on context. A strong savings habit can be protective, but taken too far, it can become fear disguised as discipline. Generosity can be healthy, but it can also become people-pleasing with a price tag.

This is where the psychology of money and your financial life become deeply personal. Your bank statements often reveal emotional patterns before your conscious mind does. Recurring food delivery during high-stress weeks, impulsive purchases after social rejection, or avoiding financial admin when feeling inadequate are not random glitches. They are behavioral signals.

When you spot the emotional function of a money habit, you gain leverage. If online shopping is serving as stress relief, the problem is not just spending. The deeper issue is emotional regulation.

Identity shapes what feels financially possible

Money is social. It does not just buy things. It buys identity, belonging, and signals.

People do not spend in a vacuum. They spend in a culture that constantly tells them what success should look like. The apartment, the skincare routine, the vacation, the wedding, the productivity setup, the “I have my life together” aesthetic – these are psychological cues as much as consumer choices.

That creates a subtle trap. If your identity becomes attached to appearing successful, cutting back can feel like personal regression rather than a practical adjustment. You are not simply reducing expenses. You are threatening a version of yourself.

This is also why income alone does not resolve financial anxiety. Someone can earn well and still feel behind if their reference group earns more, spends more, or performs success more aggressively. Social comparison distorts financial perception. Objectively stable can still feel subjectively inadequate.

A healthier question is not “What should someone like me own?” but “What am I trying to prove, and to whom?” That question cuts through a lot of expensive confusion.

The psychology of money rewards systems, not willpower

Willpower is overrated in financial life. Not useless, but unreliable. It fluctuates with stress, sleep, mood, and cognitive overload. A system beats a motivational burst almost every time.

Automatic transfers into savings work because they remove repeated decisions. Friction helps too. If your card details are not saved everywhere, impulse purchases become slightly less automatic. If your investing happens on schedule instead of as a response to headlines, fear has fewer opportunities to take over.

This sounds basic because it is. But basic does not mean weak. Many of the best financial interventions are psychologically simple: reduce temptation, automate the good behavior, and make the desired choice easier than the impulsive one.

There is a trade-off here. Highly rigid systems can backfire for people who experience them as deprivation or punishment. The goal is not to create a financial life so strict that it collapses under normal human stress. The goal is to build one with enough structure to protect you from your most predictable mistakes.

Shame keeps people financially stuck

If there is one emotion that quietly wrecks financial progress, it is shame.

Shame makes people hide. They avoid opening bills, delay asking for help, ignore debt, and tell themselves they will deal with it when they feel more in control. Unfortunately, avoidance usually makes the problem bigger, which creates more shame, and the cycle tightens.

This matters because many money problems are treated as moral failures when they are actually behavioral and emotional patterns. That does not remove personal responsibility. It changes the path forward. Shame says, “I am bad with money.” A more useful frame is, “I have learned patterns around money, and patterns can be changed.”

That distinction sounds small. Psychologically, it is enormous. Identity-based hopelessness keeps people frozen. Specific, observable behavior creates room for change.

At The Psychology of Everything, this is the more useful lens: cut through the myth that financial success is purely about discipline, and you start seeing the hidden drivers more clearly.

How to work with your mind instead of against it

A better financial life usually starts with attention, not intensity. Notice where emotion spikes. Notice what you avoid. Notice the stories you tell after spending or saving. Do you frame restraint as deprivation? Do you use spending as evidence that life is finally going well? Do you equate investing with danger because uncertainty feels intolerable?

Once you can name a pattern, you can interrupt it. That might mean setting a 24-hour pause before non-essential purchases, reviewing your transactions without self-attack, or separating self-worth from visible consumption. It may also mean getting more honest about what you actually value. Plenty of financial stress comes from funding a life that looks right from the outside but feels wrong up close.

This is where psychology becomes practical. The aim is not to become coldly rational. It is to become less manipulated by unconscious drivers. You still get to enjoy money. You still get to spend on what matters. But you do it with more awareness and less autopilot.

The mind will always be part of your financial life. There is no pure logic mode waiting to take over. But once you understand your biases, emotional triggers, and identity patterns, money stops feeling like a mysterious force and starts looking more like behavior you can study, shape, and steadily improve. That is often the point where financial change becomes real.